Credit Cards vs. Personal Loans: Which is Right for You?

In the realm of personal finance, both credit cards and personal loans offer ways to borrow money. However, they serve different purposes and come with distinct terms. Let’s break down the differences to help you determine which might be best for your financial needs.

1. Credit Cards: The Basics

Credit cards are revolving lines of credit. This means you have a set credit limit, and you can borrow up to that amount. As you repay, the available credit replenishes.

Pros:

- Flexibility: Use it for multiple purchases up to your credit limit.

- Rewards: Many cards offer cash back, points, or travel rewards.

- Grace Period: If you pay off your balance in full by the due date, you typically won’t incur interest.

Cons:

- Higher Interest Rates: Credit cards can have higher APRs compared to personal loans.

- Potential for Debt Accumulation: The flexibility can lead to overspending.

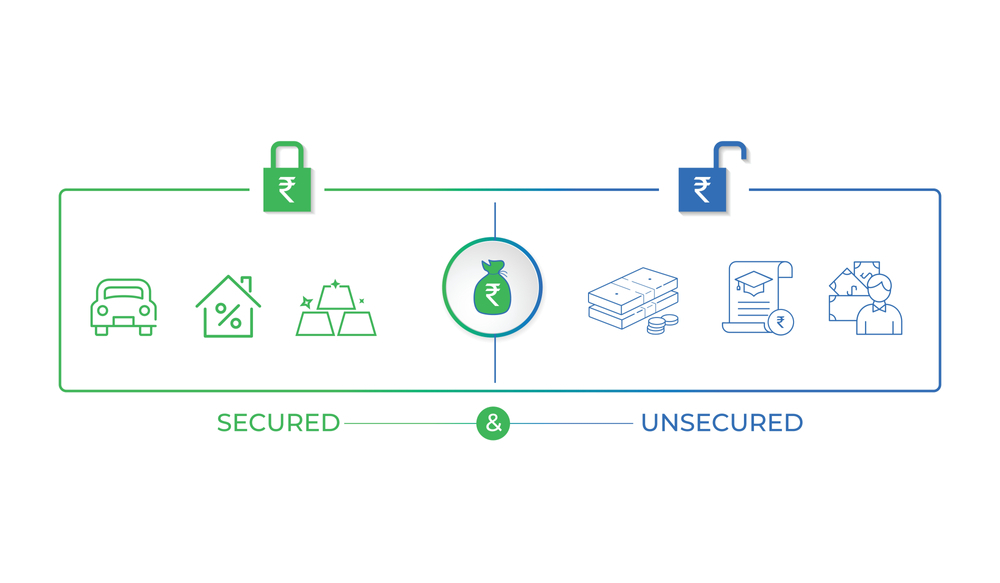

2. Personal Loans: The Basics

Personal loans are installment loans. You borrow a fixed amount and repay it in equal installments over a set term.

Pros:

- Fixed Payments: Predictable monthly payments can make budgeting easier.

- Lower Interest Rates: Often, personal loans have lower interest rates than credit cards.

- Versatility: Can be used for various purposes, from debt consolidation to home improvements.

Cons:

- Origination Fees: Some lenders charge a fee to process the loan.

- Fixed Amount: Unlike a credit card, you can’t borrow more without applying for a new loan.

3. When to Use a Credit Card

- Small Purchases: For everyday spending where you can pay off the balance monthly.

- Rewards Maximization: If you’re leveraging points or cash back.

- Short-Term Borrowing: If you’re confident in repaying the amount within the card’s grace period.

4. When to Consider a Personal Loan

- Large, One-Time Expenses: Such as medical bills or home renovations.

- Debt Consolidation: Combining high-interest debts into a single, lower-interest loan.

- Long-Term Financing: When you need more time to repay than a credit card grace period allows.

5. Key Considerations

- Interest Rates: Always compare APRs. While personal loans might offer lower rates, promotional rates on credit cards can sometimes be more competitive.

- Total Borrowing Cost: Consider fees, interest, and the loan term.

- Your Financial Habits: If you struggle with spending discipline, a credit card’s revolving nature might not be ideal.

Conclusion

Both credit cards and personal loans have their place in financial management. By understanding their unique features and assessing your financial situation and goals, you can make an informed decision that aligns with your needs and promotes financial well-being.